Futures market: LME copper was closed last Friday evening. The SHFE copper 2506 contract opened at 76,110 yuan/mt last Friday evening, with a high of 76,200 yuan/mt and a low of 75,820 yuan/mt, closing at 75,900 yuan/mt. The overall trend showed initial fluctuations followed by a downward fluctuation, with a change of -90 yuan, a decrease of 0.12%. The trading volume was 39,206 lots, and the open interest was 160,221 lots, with a daily increase of -3,262 lots, a daily change rate of -2.00%.

[SMM Copper Morning Meeting Summary] News: (1) Tariffs - The Trump administration has begun discussing the establishment of a task force to urgently address the crisis of imposing additional tariffs on China. Trump does not want tariffs to continue to rise and claims that an agreement with China will be reached within one month; US media: Trump's "own people" are also restless, secretly hoping that the US Supreme Court will halt the tariff war. (2) The US announced final measures against China's shipbuilding and other fields, and the Ministry of Commerce responded: It will closely monitor the US's relevant moves and will resolutely take necessary measures to safeguard its own rights and interests. The China Shipowners Association and other industry associations have intensively voiced their opinions.

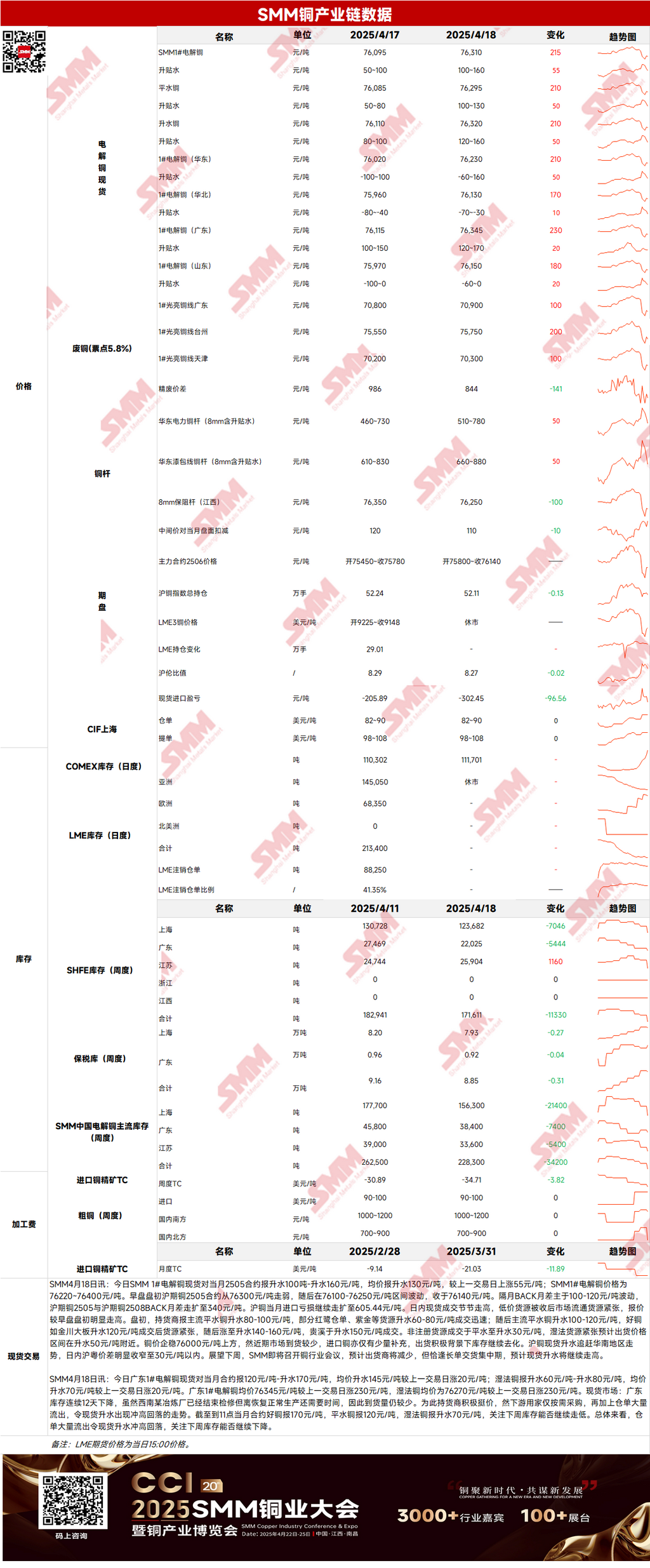

Spot: (1) Shanghai: On April 18, SMM #1 copper cathode spot prices against the front-month 2505 contract were at a premium of 100-160 yuan/mt, with an average premium of 130 yuan/mt, up 55 yuan/mt from the previous trading day. Copper prices stabilized above 76,000 yuan/mt, but recent market arrivals were limited, and imported copper was only supplemented in small quantities. Against the backdrop of active shipments, inventories continued to decline. Shanghai spot copper premiums followed the trend in South China, narrowing significantly to within 30 yuan/mt on April 8. Looking ahead to this week, SMM is about to hold a copper industry conference, and it is expected that suppliers will decrease, but coinciding with the concentrated delivery period of long-term contracts, spot premiums are expected to continue to rise.

(2) Guangdong: On April 18, Guangdong #1 copper cathode spot prices against the front-month contract were at a premium of 120-170 yuan/mt, with an average premium of 145 yuan/mt, up 20 yuan/mt from the previous trading day. Overall, the large outflow of warrants caused spot premiums to jump initially and then pull back. Attention will be paid to whether inventories can continue to decline this week.

(3) Imported copper: On April 18, single prices were at 82-90 $/mt, QP May, with the average price unchanged from the previous trading day; B/L prices were at 98-108 $/mt, QP May, with the average price unchanged from the previous trading day. EQ copper (CIF B/L) was at 55-65 $/mt, QP May, with the average price unchanged from the previous trading day, with reference to shipments arriving in mid to late April. On April 18, LME copper was closed, and due to the inability to price, market transactions were scarce. A small number of B/Ls were still offered, with no significant fluctuations in the price center. It was heard that pyrometallurgy B/Ls for late April were offered at 100-105 $, and three brands for early May were offered at 115-120 $, QP May. Domestic warrants were offered at around 95 $/5 QP. EQ B/Ls for mid to late April were offered at 60-70 $/5 QP, but transactions were hard to find. Overall, EQ remained firm, but market trading volume significantly decreased. Due to the sharp rise in domestic trade premiums, the SHFE/LME price ratio has room for support, and it is expected that Yangshan copper premiums will continue to rise this week.

(4) Secondary copper: On April 18, secondary copper raw material prices rose by 100 yuan/mt MoM, with Guangdong bare bright copper prices at 70,800-71,000 yuan/mt, up 100 yuan/mt MoM from the previous trading day. The price difference between copper cathode and copper scrap was 844 yuan/mt, down 142 yuan/mt MoM. The price difference between copper cathode rod and secondary copper rod was 535 yuan/mt. According to the SMM survey, secondary copper import traders stated that after stopping purchases from the US, recent European sources have also decreased, due to reduced local production and increased local consumption in Europe, leading to secondary copper suppliers' quotations far exceeding reasonable ranges. It is expected that April purchases will be only 50% of March's.

(5) Inventories: On April 18, LME copper inventories remained unchanged; on April 18, SHFE warrant inventories decreased by 12,027 mt to 65,097 mt.

Prices: On the macro front, Trump criticized businessmen who oppose tariffs as not being good at business, but what they are really not good at is politics. Trump listed eight non-tariff "cheating" methods, naming Japan and the EU. Meanwhile, the Trump administration has begun discussing the establishment of a task force to urgently address the crisis of imposing additional tariffs on China. Trump does not want tariffs to continue to rise and claims that an agreement with China will be reached within one month. US media: Trump's "own people" are also restless, secretly hoping that the US Supreme Court will halt the tariff war. US media reported that over 700 protests erupted across the US, opposing the US government's large-scale layoffs of federal employees, agency cuts, and immigration expulsion policies. Under the repeated tariff policies, copper prices fluctuated at highs. On the fundamental side, recent market arrivals were limited, and imported copper supplements were also limited. Against the backdrop of active shipments, inventories continued to decline. This week, SMM is about to hold a copper industry conference, and it is expected that suppliers will decrease, but coinciding with the concentrated delivery period of long-term contracts, spot premiums are expected to continue to rise. Overall, it is expected that today's copper prices will have limited upward momentum.

Click to view the SMM Metal Database

[The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided in this article is for reference only. This article does not constitute direct advice for investment research decisions. Clients should make decisions cautiously and not use this to replace independent judgment. Any decisions made by clients are unrelated to SMM.]